Understanding Interest Rates: A Comprehensive Guide For Your Financial Future

Mar 19 2025

Interest rates play a crucial role in shaping the global economy and influencing personal financial decisions. Whether you're saving money, borrowing for a mortgage, or investing in the stock market, understanding interest rates is essential. They affect everything from credit card payments to business loans and government policies. In this article, we will explore the ins and outs of interest rates, helping you make informed decisions about your finances.

Interest rates are one of the most important factors in modern financial systems. They dictate how much it costs to borrow money and how much you can earn by saving or investing. Whether you're an individual, a business owner, or a policymaker, understanding interest rates ensures that you can navigate financial landscapes effectively.

This article will delve into the concept of interest rates, their types, how they are determined, and their impact on the economy. We'll also discuss strategies to manage interest rates and provide actionable advice to help you make the most of your financial opportunities. Let's get started!

Read also:Jaden Hardy News Available Wednesday Ndash The Rising Star Making Waves

Table of Contents

- What Are Interest Rates?

- Types of Interest Rates

- Factors Affecting Interest Rates

- How Interest Rates Impact the Economy

- Central Banks and Interest Rates

- Calculating Interest Rates

- Managing Interest Rates

- Historical Interest Rate Trends

- Common Misconceptions About Interest Rates Conclusion

What Are Interest Rates?

Interest rates refer to the cost of borrowing money or the return on saved or invested funds, expressed as a percentage of the principal amount. Essentially, interest rates represent the price of money. For borrowers, they indicate how much extra they will need to pay back, while for lenders or savers, they signify the earnings they can expect.

Interest rates can vary depending on the type of loan, the borrower's creditworthiness, and the overall economic conditions. They are typically set by central banks, financial institutions, or market forces. Understanding the basics of interest rates is essential for anyone looking to manage their finances effectively.

Key Characteristics of Interest Rates

- Expressed as an annual percentage rate (APR).

- Can be fixed or variable, depending on the loan agreement.

- Linked to inflation, economic growth, and monetary policies.

Types of Interest Rates

Interest rates come in various forms, each serving a specific purpose in the financial world. The most common types include nominal interest rates, real interest rates, and effective interest rates. Additionally, there are short-term and long-term interest rates, which cater to different borrowing and lending needs.

Nominal vs. Real Interest Rates

Nominal interest rates represent the stated interest rate without accounting for inflation. On the other hand, real interest rates adjust for inflation, providing a more accurate reflection of the purchasing power of borrowed or saved money.

Short-Term and Long-Term Interest Rates

Short-term interest rates typically apply to loans or investments lasting less than one year, while long-term interest rates cover periods exceeding one year. Central banks often influence short-term rates through monetary policy, whereas market forces primarily determine long-term rates.

Factors Affecting Interest Rates

Interest rates are influenced by a variety of factors, including economic conditions, inflation, and monetary policies. These factors interact in complex ways to determine the level of interest rates at any given time.

Read also:Mavericks Vs Pacers A Deep Dive Into The Rivalry Game Analysis And Key Players

Economic Conditions

Economic growth, unemployment rates, and consumer confidence all play a role in shaping interest rates. For instance, during periods of strong economic growth, interest rates may rise to prevent overheating and control inflation.

Inflation

Inflation erodes the purchasing power of money, and central banks often raise interest rates to combat rising inflation. Conversely, during periods of deflation or low inflation, interest rates may be lowered to stimulate spending and investment.

Monetary Policies

Central banks, such as the Federal Reserve in the United States or the European Central Bank, use monetary policy tools to influence interest rates. By adjusting the supply of money and setting benchmark rates, they aim to achieve economic stability and price stability.

How Interest Rates Impact the Economy

Interest rates have far-reaching effects on the economy, influencing everything from consumer spending to business investment. When interest rates are low, borrowing becomes cheaper, encouraging businesses to expand and consumers to make big-ticket purchases. Conversely, high interest rates discourage borrowing and spending, which can slow down economic growth.

Impact on Consumers

For consumers, interest rates affect the cost of mortgages, car loans, and credit card payments. Lower interest rates can lead to increased spending and borrowing, boosting economic activity. However, if interest rates rise too quickly, it can strain household budgets and reduce disposable income.

Impact on Businesses

Businesses rely on borrowing to finance operations, expand facilities, and invest in new projects. Low interest rates make it easier for companies to access capital, fostering innovation and growth. High interest rates, however, can increase borrowing costs, potentially stifling business expansion.

Central Banks and Interest Rates

Central banks play a pivotal role in setting interest rates and managing monetary policy. By adjusting benchmark rates, they aim to maintain price stability, promote economic growth, and ensure full employment. Central banks use a variety of tools, such as open market operations and reserve requirements, to influence interest rates and achieve their policy objectives.

How Central Banks Set Interest Rates

Central banks set interest rates based on economic data, inflation forecasts, and global financial conditions. They monitor key indicators such as GDP growth, employment rates, and inflation levels to determine the appropriate level of interest rates. Through regular policy meetings, central banks communicate their decisions and provide guidance on future rate movements.

Calculating Interest Rates

Calculating interest rates involves understanding the terms of a loan or investment. Whether you're dealing with simple interest, compound interest, or annual percentage rates (APR), the process requires careful attention to detail. Below are some common methods for calculating interest rates:

Simple Interest Formula

Simple interest is calculated using the formula:

I = P × r × t

Where:

- I = interest

- P = principal amount

- r = annual interest rate (in decimal form)

- t = time (in years)

Compound Interest Formula

Compound interest takes into account the interest accrued on both the principal and previously accumulated interest. The formula for compound interest is:

A = P(1 + r/n)nt

Where:

- A = total amount (principal + interest)

- P = principal amount

- r = annual interest rate (in decimal form)

- n = number of compounding periods per year

- t = time (in years)

Managing Interest Rates

Effectively managing interest rates requires a solid understanding of financial principles and market dynamics. Whether you're a borrower or an investor, there are strategies you can employ to mitigate the risks associated with fluctuating interest rates.

For Borrowers

- Opt for fixed-rate loans when interest rates are low.

- Monitor market trends and consider refinancing when rates drop.

- Maintain a good credit score to secure favorable interest rates.

For Investors

- Diversify your portfolio to reduce exposure to interest rate risks.

- Consider investing in bonds or other fixed-income securities when rates are expected to rise.

- Stay informed about central bank policies and economic indicators.

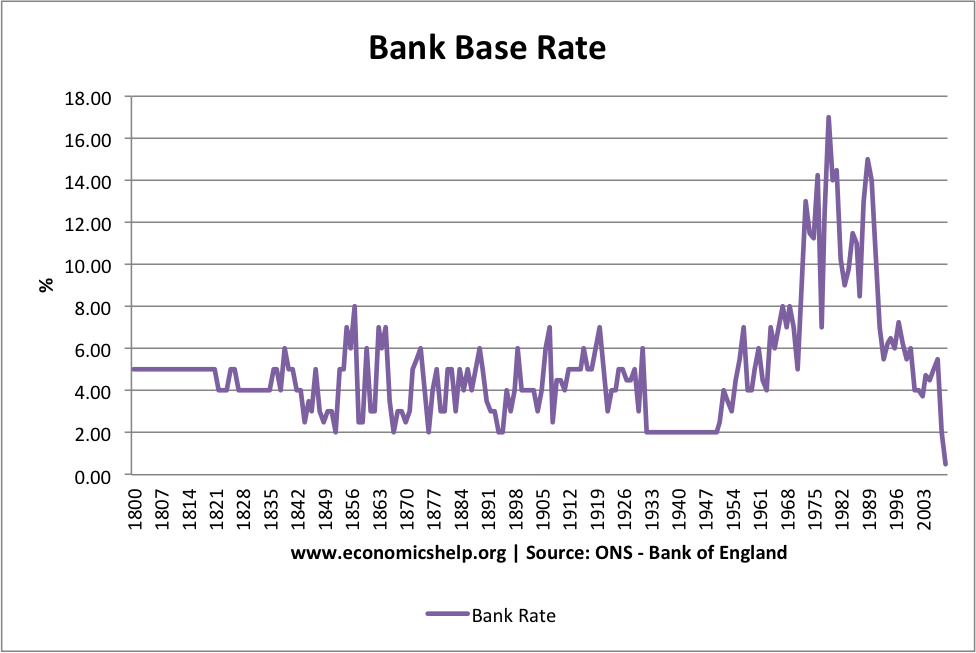

Historical Interest Rate Trends

Examining historical interest rate trends provides valuable insights into how economic conditions and monetary policies have evolved over time. For example, during the 1980s, interest rates in the United States reached historic highs as the Federal Reserve battled rampant inflation. In contrast, the post-2008 financial crisis era saw near-zero interest rates as central banks sought to stimulate economic recovery.

Key Historical Events

- 1980s: Double-digit interest rates in response to high inflation.

- 2008 Financial Crisis: Near-zero interest rates to stabilize the economy.

- 2020 Pandemic: Central banks worldwide cut rates to unprecedented levels to mitigate economic fallout.

Common Misconceptions About Interest Rates

Despite their importance, interest rates are often misunderstood. Below are some common misconceptions and the truths behind them:

Misconception 1: Lower Interest Rates Always Mean Better Borrowing Conditions

While lower interest rates reduce borrowing costs, they can also indicate economic uncertainty or deflationary pressures. Borrowers should consider the broader economic context before making financial decisions.

Misconception 2: Interest Rates Are Uniform Across All Loans

Interest rates vary significantly depending on the type of loan, the borrower's creditworthiness, and market conditions. It's essential to compare rates and terms carefully before committing to a loan or investment.

Conclusion

Interest rates are a fundamental aspect of modern financial systems, influencing everything from personal savings to global economic policies. By understanding the different types of interest rates, the factors affecting them, and their impact on the economy, you can make more informed financial decisions.

We encourage you to take action by reviewing your current financial situation and exploring opportunities to optimize your interest rate strategies. Don't hesitate to share your thoughts in the comments section or explore other articles on our site for further insights into personal finance and economic trends.